Introduction

I remember sitting on my kitchen floor in 2019, surrounded by three different “Explanation of Benefits” (EOB) statements that made absolutely no sense. I had a $1,200 bill for a 15-minute ER visit where they didn’t even give me a bandage. I had insurance or so I thought.

That was the day I realized that health insurance basics aren’t just “basic” they are the gatekeepers to your financial freedom.

In this guide, we are going to deconstruct the labyrinth of the healthcare system. Whether you are choosing a plan for the first time, navigating a job change, or trying to figure out how to choose the right health insurance plan during a mid-life crisis, this is your map. We’re going deep beyond the definitions into the strategy of health wealth.

Part 1: The Philosophy of Coverage: Why “Basic” is a Misnomer

When we talk about health insurance basics, we often focus on the vocabulary. But the “basic” philosophy you must understand is Risk Transfer. Insurance is a contract where you pay a known, small amount (the premium) to avoid an unknown, catastrophic amount (a $150,000 heart surgery). The problem is that the “contract” is written in a language designed to be skimmed, not understood.

The Evolution of the System

In the 1950s, health insurance was “Major Medical.” It only kicked in if you were basically at death’s door. Today, it’s a managed care system. This means the insurance company isn’t just a payer; they are a “gatekeeper.” They decide which drugs you can take and which specialists are “worthy” of your visit.

Understanding this power dynamic is the first step in mastering health insurance basics. You aren’t just a patient; you are a policyholder in a multi-billion dollar negotiation.

Part 2: The Anatomy of Your Plan The “Guts” of the Policy

If you want to know how to choose the right health insurance plan, you have to look at the “Summary of Benefits and Coverage” (SBC). Every plan is required by law to have one.

The Premium: The Silent Budget Killer

The premium is the most visible cost, but it’s often a distraction.

-

The Trap: Choosing the lowest premium because it “saves money” monthly.

-

The Reality: If you have a $9,000 deductible, you don’t actually have insurance for daily life; you have “bankruptcy protection.”

The Deductible: The Wall Between You and Coverage

The deductible is the amount you pay before the insurance company pays a dime.

-

Embedded vs. Aggregate Deductibles: If you have a family plan, this is huge. An embedded deductible means if one person hits their individual limit, their coverage starts. An aggregate deductible means the entire family must hit the total limit before anyone gets coverage.

Coinsurance: The “Split”

Once you hit your deductible, you enter the “Coinsurance Phase.” This is usually expressed as a ratio (e.g., 80/20).

-

The 80/20 Rule: The insurance pays 80%, you pay 20%.

-

The Danger: 20% of a $100,000 surgery is still $20,000. This is why the next term is the most important one in this entire guide.

The Out-of-Pocket Maximum (OOPM): Your Holy Grail

The OOPM is the legal limit on how much you can spend in a year on “covered” services.

-

What counts: Deductibles, copays, and coinsurance.

-

What doesn’t count: Your premiums, or “out-of-network” balance billing.

-

Strategy: If you know you have a major surgery coming up, the OOPM is the only number that matters. Buy the plan with the lowest OOPM, even if the premium is higher.

Part 3: Choosing Your Network PPO, HMO, EPO, and the “Alphabet Soup”

One of the biggest hurdles in how to choose the right health insurance plan is the network. A “Network” is a group of doctors who have signed a contract with the insurance company to accept lower rates.

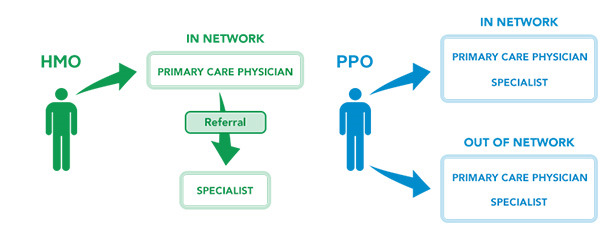

The HMO (Health Maintenance Organization)

-

Pros: Lowest premiums, predictable costs.

-

Cons: You must have a Primary Care Physician (PCP). You must get a referral to see a specialist. If you go out of network, you pay 100%.

-

Who it’s for: People who have a trusted local doctor and don’t travel much.

The PPO (Preferred Provider Organization)

-

Pros: Flexibility. No referrals needed. You can see a specialist in another state if they are in the network.

-

Cons: Higher premiums.

-

Who it’s for: People who want autonomy or have complex health needs requiring multiple specialists.

The EPO (Exclusive Provider Organization)

-

Pros: Cheaper than a PPO, but you don’t need referrals.

-

Cons: No out-of-network coverage at all.

-

Who it’s for: People in major metros with massive hospital systems (like Kaiser or Mayo Clinic) where everything they need is under one roof.

The POS (Point of Service)

-

Pros: A hybrid. You have a PCP but can go out of network if you’re willing to pay more.

-

Cons: Confusing paperwork.

-

Who it’s for: Rare these days, but good for those who want a “safety valve” to see a specific out-of-state expert.

Part 4: A Deep Dive Comparison Table

| Feature | Bronze Plan | Silver Plan | Gold Plan |

| Monthly Premium | Lowest ($) | Mid ($$) | High ($$$) |

| Deductible | Very High | Moderate | Low |

| Primary Use Case | Emergency only | General family use | High medical needs |

| Cost Sharing | You pay 40% | You pay 30% | You pay 20% |

| Subsidies | Premium tax credits | Credits + CSRs | Premium tax credits |

Part 5: The “Hidden” Rules of Prescription Drugs

When people study health insurance basics, they often forget the “Formulary.” This is the list of drugs your insurance covers.

The Tier System

-

Tier 1: Generics (Cheapest).

-

Tier 2: Preferred Brands.

-

Tier 3: Non-Preferred Brands.

-

Tier 4: Specialty Drugs (Biologics, cancer meds extremely expensive).

Real-world tip: Before you sign up for a plan, search their “Online Formulary” for your specific medications. I once saw a patient switch to a “cheaper” plan only to find their $50 insulin shot was now $600 because it was “off-formulary.”

For more on how to navigate prescription costs, the FDA’s guide on Generic Drugs is an essential read to understand why Tier 1 is your best friend.

Part 6: Telehealth: The 2026 Frontier

As a senior strategist in the telehealth niche, I cannot stress this enough: Telehealth is no longer an “extra.” It is a core pillar of health insurance basics.

In 2026, many “Virtual-First” plans are hitting the market. These plans often have $0 copays for virtual visits.

-

Why use them? For sinus infections, rashes, mental health therapy, and prescription refills.

-

The benefit: You save the $150 “Facility Fee” that brick-and-mortar clinics charge just for walking through the door.

Part 7: Step-by-Step: How to Choose the Right Health Insurance Plan

If you are staring at the portal right now, follow this 5-step framework:

Step 1: The “Past Year” Audit

Look at your bank statements. How many times did you see a doctor? How many prescriptions did you fill? If you spent less than $500 on healthcare, you are a “Low User.” If you spent over $2,000, you are a “High User.”

Step 2: Check the “Doctor Lock”

Do you have a doctor you love? Go to their website or call them. Ask for their NPI (National Provider Identifier). Use that number to search the insurance company’s directory. Names can be similar; NPIs are unique.

Step 3: Calculate the “Worst Case Scenario”

Add your total annual premiums to your Out-of-Pocket Maximum.

This is the most you will pay if you get hit by a bus. Compare this number across plans. Often, the Gold plan has a lower total risk than the Bronze plan.

Step 4: Evaluate the HSA Opportunity

If you are healthy and have savings, a High Deductible Health Plan (HDHP) with an HSA is a triple-tax-advantaged miracle.

-

Money goes in tax-free.

-

Grows tax-free.

-

Comes out tax-free for health costs.

-

Bonus: After age 65, it acts like a traditional IRA.

Step 5: Look for “Value-Added” Benefits

Does the plan offer a free gym membership? A reward for getting a flu shot? $200 back for completing a health assessment? These small perks can offset the cost of the premium.

Part 8: Navigating the “No Surprises Act” and Billing Errors

Even with a firm grasp of health insurance basics, the system can fail you. Medical billing is notoriously error-prone.

Fact: It is estimated that up to 80% of medical bills contain at least one error.

How to Fight Back

-

Request an Itemized Bill: Don’t pay a “Balance Due” statement. Demand the codes (CPT codes).

-

Check for “Unbundling”: This is when a provider charges for three separate things that should have been one “bundle.”

-

The No Surprises Act: If you go to an in-network hospital but an out-of-network doctor treats you, they cannot bill you more than the in-network rate. This is federal law.

For a deeper dive into your rights, the Consumer Financial Protection Bureau (CFPB) provides excellent documentation on how to dispute medical debt.

Part 9: Specialized Coverage Dental, Vision, and Beyond

Standard health insurance rarely covers “the head.”

-

Dental: Usually a separate policy with a low “Annual Maximum” (often $1,500).

-

Vision: Mostly pays for one exam and a portion of frames.

-

Why buy them? Dental insurance is almost always worth it for the two free cleanings alone, which usually cost more than the annual premium.

Part 10: Frequently Asked Questions

What is the difference between “In-Network” and “Out-of-Network”?

“In-network” means the doctor has agreed to a pre-negotiated discount. “Out-of-network” means the doctor can charge whatever they want, and your insurance may cover 0% of it.

Can I stay on my parent’s plan until 26 if I’m married?

Yes. Under current health insurance basics laws, your marital status or tax dependency doesn’t matter. You can stay on until your 26th birthday.

What if I can’t afford any plan?

Check your state’s Medicaid eligibility. In many states, if you earn below 138% of the federal poverty level, you qualify for nearly free coverage. Alternatively, look for “Catastrophic Plans” if you are under 30.

Does health insurance cover mental health?

Yes. Under the Mental Health Parity and Addiction Equity Act, insurance companies must treat mental health and substance use disorder benefits the same way they treat medical and surgical benefits.

Conclusion: Your Health is Your Wealth

We have covered a lot of ground from the “Metal Tiers” to the “Alphabet Soup” of networks and the hidden power of the HSA. But if you take away only one thing from this guide, let it be this: Health insurance is a product you are buying. You are the customer. You have the right to ask questions, to dispute bills, and to shop around. Understanding health insurance basics gives you the leverage to ensure that a medical emergency remains a health event, not a financial one.

Ready to dive deeper into healthy side of wellness?

Next Page: 7 Essential Healthy Living Tips You Need to Know to Protect Your Health in a Modern World

Sources & References

- HealthCare.gov — Understanding Health Insurance Basics

- FDA — Generic Drugs Overview

- CMS — No Surprises Act Overview

- Consumer Financial Protection Bureau — Disputing Medical Debt

- IRS — HSA Tax Advantages

- Mental Health Parity and Addiction Equity Act — SAMHSA Overview

- Medicaid.gov — Eligibility Requirements