Introduction

Picture this: You’ve just landed your first real job, or you’re switching employers, and someone slides a benefits enrollment packet across the desk. It’s forty pages of dense text riddled with words like “out-of-pocket maximum,” “formulary,” and “explanation of benefits.” Your eyes glaze over. You nod anyway, pick a plan, and pray you chose correctly.

You’re not alone. Health insurance terminology is, to put it diplomatically, a masterpiece of obfuscation. Whether you’re navigating an employer plan in the United States, weighing private coverage against Canada’s provincial systems, or deciding whether BUPA is worth the cost in the UK, the language of health insurance reads like a foreign dialect — one that happens to have enormous financial consequences if you misread it.

This guide exists to change that. Think of it as your personal translator for one of the most consequential financial products you’ll ever buy.

Why Health Insurance Terms Feel So Confusing (And Why It’s Not Your Fault)

The insurance industry didn’t develop its vocabulary to make your life easier. It evolved across decades of regulatory frameworks, actuarial science, and legal fine-tuning — none of which prioritized everyday readability. According to Families USA, many Americans, Canadians, and Britons struggle to accurately define even the most basic health insurance concepts, despite paying for coverage every single month.

The result? People unknowingly choose the wrong plan, miss out on covered benefits, and get blindsided by bills they thought their insurer would handle. Understanding health insurance terms isn’t just an academic exercise — it’s a financial survival skill.

So let’s get into it.

The Core Health Insurance Terms You Absolutely Need to Know

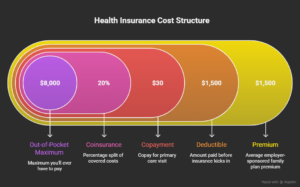

1. Premium

Your premium is what you pay every month just to have insurance — whether you use it or not. Think of it like a subscription fee. In the US, the average employer-sponsored family plan carries a monthly premium well into four figures, with employees typically covering a significant portion of that cost. In Canada, if you’re buying supplemental private coverage (since provincial health plans cover the basics), your premium depends on your province, age, and what you’re covering. In the UK, private insurers like BUPA and AXA Health charge premiums that vary based on your age, chosen coverage level, and whether you’re adding extras like dental.

Here’s the key insight most people miss: a lower premium almost always means higher costs when you actually need care. The premium is just the entry fee. The real money game happens below.

2. Deductible

The deductible is the amount you pay out of your own pocket before your insurance kicks in and starts sharing the costs. If your deductible is $1,500, you pay the first $1,500 of covered medical expenses each year. After that, your insurer steps in.

In the US, the Bureau of Labor Statistics defines the deductible as the threshold of covered expenses an enrollee must meet before the plan starts paying benefits. High-deductible health plans (HDHPs) have become increasingly common, often paired with Health Savings Accounts (HSAs) that let you set aside pre-tax money for medical costs.

In Canada, provincial health plans don’t typically have deductibles for covered services — but your supplemental private plan (covering things like dental, vision, and prescription drugs) very likely does. In the UK, private health insurance through providers like BUPA uses the term “excess” instead of deductible, but it works the same way.

3. Copayment (Copay) and Coinsurance

Once you’ve met your deductible, you usually still share costs with your insurer through one of two mechanisms:

- Copay: A fixed dollar amount you pay for a specific service. “Your copay for a primary care visit is $30” means you hand over $30, the insurer covers the rest. Simple.

- Coinsurance: A percentage split. If your coinsurance is 20%, you pay 20% of the covered cost; the insurer pays 80%. This one can surprise people — especially for expensive procedures.

The WPS Health glossary describes coinsurance as one of the most misunderstood cost-sharing mechanisms, precisely because the dollar amount varies based on the total cost of service rather than a fixed fee.

4. Out-of-Pocket Maximum

This is your financial safety net. The out-of-pocket maximum (or out-of-pocket limit) is the most you’ll ever have to pay for covered services in a given plan year. Once you hit this ceiling, your insurer covers 100% of covered services for the rest of the year.

In the US, federal law sets annual limits on how high this cap can go for marketplace plans. In Canada and the UK, the concept functions similarly in private supplemental coverage, though the structure varies by insurer and plan tier.

Here’s the practical wisdom: your out-of-pocket maximum is the single most important number for estimating your worst-case financial exposure in a bad health year. When comparing plans, always look at this figure alongside the premium.

5. Network: In-Network vs. Out-of-Network

Your insurance plan has a network — a group of doctors, hospitals, specialists, and facilities that have agreed to contracted rates with your insurer. Staying in-network means your insurer and that provider have pre-negotiated what each service costs. Going out-of-network means all bets are off, and you could face dramatically higher bills — or no coverage at all.

This is particularly crucial in the US, where network rules are strict and the financial penalties for going out-of-network can be severe. As noted by the Centers for Medicare & Medicaid Services, understanding whether your preferred doctors and hospitals are in your plan’s network before you enroll can save you thousands.

In the UK, private insurers like BUPA operate their own networks of approved specialists and facilities. In Canada, network concepts apply primarily to supplemental dental and vision plans.

6. Explanation of Benefits (EOB)

After you receive medical care, your insurer sends you an Explanation of Benefits — a document breaking down what was charged, what your insurer covered, and what you owe. This is not a bill. It’s a receipt-style statement showing how your claim was processed.

Reading your EOB is like checking a restaurant receipt for errors — worth doing, especially for significant procedures. Billing errors in healthcare are more common than most people realize, and catching them requires knowing what you’re looking at.

7. Pre-existing Condition

A pre-existing condition is any health condition you had before your coverage began. In the US, the Affordable Care Act prohibits most insurers from denying coverage or charging higher premiums based on pre-existing conditions. In Canada, provincial plans cover all residents regardless of health history; however, private supplemental insurers may exclude or limit coverage for conditions diagnosed before enrollment. In the UK, private insurers like BUPA may or may not cover pre-existing conditions depending on the type of policy — moratorium policies, for instance, typically exclude pre-existing conditions for a set period.

8. Formulary

A formulary is your insurer’s approved list of covered prescription drugs, organized into tiers. Tier 1 might include generic drugs with low copays; Tier 3 might include brand-name specialty drugs with significant cost-sharing. Understanding your plan’s formulary before choosing coverage — and before your doctor prescribes something — can save you from sticker shock at the pharmacy counter.

Health Insurance Terms at a Glance: A Comparison Table

| Term | US Context | Canada Context | UK Context |

|---|---|---|---|

| Premium | Monthly payment to insurer | Paid for private supplemental plans | Monthly fee for private insurers (BUPA, AXA) |

| Deductible | Applies to most private plans | Common in supplemental dental/drug plans | Called “excess” in UK private insurance |

| Copay | Fixed fee per service | Common in supplemental plans | Less common; often flat or percentage |

| Out-of-Pocket Max | Federally capped for marketplace plans | Varies by private plan | Varies by insurer |

| Network | Critical in most US plans | Applies mainly to supplemental plans | BUPA/AXA maintain their own networks |

| Pre-existing Conditions | Covered by law in ACA plans | Covered by provincial plans; may be excluded in private | Varies; moratorium vs. full medical underwriting |

| Formulary | Drug tiers; affects copay | Common in drug benefit plans | Listed in policy documents |

Frequently Asked Questions About Health Insurance Terms

What is the cheapest health insurance in Canada?

Canada’s provincial and territorial health plans cover most essential medical services at no direct cost to residents — so for core coverage, cost isn’t the issue. Where spending enters the picture is supplemental private insurance, which covers things provincial plans don’t: dental care, prescription drugs, vision, and paramedical services like physiotherapy.

For supplemental coverage, providers like Manulife, Sun Life, and Blue Cross are among the most recognized names. Which is better — Manulife or Blue Cross? Sun Life or Blue Cross? — depends heavily on what you need covered and your province of residence. Monthly premiums for basic individual supplemental plans can start as low as a few dozen dollars, but comprehensive family coverage can run considerably higher. If you’re asking whether it’s worth buying private health insurance in Canada, the answer for most working adults is yes — especially for prescription drug coverage, which provincial plans don’t fully cover for many demographics.

You can indeed buy your own health insurance in Canada independently of an employer. Direct-to-consumer plans from providers like Manulife or Sun Life are widely available.

Can a diabetic get health insurance?

Yes — and this is an area where the rules differ meaningfully across the three countries covered here.

In the United States, the Affordable Care Act prohibits insurers on the marketplace from denying coverage or raising premiums because of a diabetes diagnosis. So yes, you can absolutely get health insurance if you’re diabetic.

In Canada, provincial plans cover all residents including those with diabetes. Private supplemental plans may have waiting periods or exclusions for diabetes-related complications, so reading the fine print matters.

In the UK, NHS coverage is universal regardless of health status. Private insurers may exclude pre-existing conditions including diabetes, depending on the policy type. Moratorium-based policies often exclude conditions diagnosed within a certain number of years before enrollment.

People with diabetes may wonder whether their condition will affect premiums — the answer in the UK private market is often yes. Whether insurance goes up because of diabetes depends on the insurer and underwriting approach. Some conditions can also affect life insurance eligibility and pricing; it’s worth consulting a specialist broker who understands how different insurers approach diabetes.

Does Canada Life cover LASIK surgery?

LASIK and vision correction procedures are generally considered elective, which means most provincial health plans don’t cover them. Private supplemental insurers, including Canada Life, typically include vision benefits as part of their plans — but whether LASIK specifically is covered depends on your plan tier and the exact policy language.

What Canada Life plans more reliably cover includes prescription glasses and contact lenses, up to an annual or biennial benefit limit. The question of whether LASIK is worth the investment — especially after 40, when presbyopia may begin to affect vision — is a conversation worth having with an ophthalmologist before committing.

For the UK, neither the NHS nor most private insurers routinely cover LASIK as it’s classified as cosmetic/elective. Dental implants follow similar logic: generally not covered by standard insurance in Canada or the UK without specific add-on riders.

What is the best health insurance in the UK?

The UK’s National Health Service provides universal coverage, so private health insurance is genuinely supplemental here — it buys you things like faster specialist access, private rooms, and choice of consultant. The most commonly cited private providers are BUPA, AXA Health, Aviva, and Vitality.

BUPA is frequently top-ranked for its breadth of specialist network and customer service, though AXA Health also earns high marks. Whether BUPA is worth it for you depends on your income, how much you value speed and choice over NHS-provided care, and whether your employer offers it as a benefit (many large UK employers do).

For those wondering about cost: BUPA premiums vary significantly by age, health status, and coverage level. Entry-level individual plans can start in the range of £30–50 per month, while comprehensive family coverage runs considerably higher. Does BUPA cover pre-existing conditions? Policies with full medical underwriting may exclude them; moratorium policies exclude conditions from the past few years but may cover them later if symptom-free.

Is health insurance better than NHS? Not better — different. The NHS covers you comprehensively; private insurance augments speed, comfort, and choice. For routine and emergency care, the NHS remains excellent. For elective procedures with waiting lists, private coverage can be genuinely valuable.

How do I decide which health insurance is best for me?

The right plan hinges on three variables that only you can weigh: your budget, your expected healthcare usage, and your risk tolerance.

Eleff Law’s plain-language guide to health insurance terms suggests a simple mental model: if you’re generally healthy and rarely see doctors, a high-deductible plan with a low premium and a Health Savings Account can make financial sense. If you have ongoing health needs, a plan with higher premiums but lower cost-sharing (lower deductible, lower coinsurance, lower out-of-pocket max) often works out to less total spending over the year.

In all three countries, the calculus is the same: add up your worst-case scenario costs (premium × 12 + out-of-pocket maximum) for each plan you’re comparing. That number tells you the ceiling of your financial exposure. Then pick the plan where that ceiling — combined with the coverage you actually need — represents the best value.

Advanced Health Insurance Terms Worth Knowing

Prior Authorization

Some services require your insurer to approve them before you receive care. Skip this step, and your insurer may deny the claim. Always check whether a procedure, specialist visit, or prescription drug requires prior authorization before scheduling.

Explanation of Benefits vs. Bill

As mentioned, your EOB is not a bill. Many patients pay an EOB thinking it’s an invoice, then receive the actual bill from the provider and pay again. Read each document carefully and don’t pay until you receive an actual bill from the provider.

Open Enrollment and Special Enrollment Periods

In the US, you can only sign up for or change marketplace health plans during open enrollment — typically a set window each fall — unless you qualify for a special enrollment period triggered by life events like job loss, marriage, or moving. In Canada and the UK, private supplemental plans often allow enrollment year-round, though some apply waiting periods for pre-existing conditions.

HSA, FSA, and HRA (US-Specific)

These are tax-advantaged accounts tied to health spending:

- HSA (Health Savings Account): Available with high-deductible plans; funds roll over year to year and can be invested

- FSA (Flexible Spending Account): Employer-sponsored; use-it-or-lose-it rules apply (with some grace period options)

- HRA (Health Reimbursement Arrangement): Employer-funded; reimburses employees for qualified medical expenses

Understanding which account you have and how to maximize it is one of the clearest ways to reduce your annual healthcare spending.

Key Differences in Health Insurance Across US, Canada, and UK

| Factor | United States | Canada | United Kingdom |

|---|---|---|---|

| Baseline Coverage | Employer, marketplace, or government programs (Medicaid, Medicare) | Universal provincial plans for core services | NHS covers all residents |

| Private Insurance Role | Primary coverage for most working adults | Supplemental (dental, drugs, vision) | Supplemental (speed, choice, comfort) |

| Major Providers | UnitedHealth, Cigna, Aetna, Blue Cross | Manulife, Sun Life, Blue Cross, Canada Life | BUPA, AXA Health, Aviva, Vitality |

| Enrollment Model | Open enrollment + SEPs; employer-based | Year-round for most supplemental plans | Year-round for private insurers |

| Pre-existing Conditions | Must be covered in ACA plans | Covered by provincial plans; may be limited privately | Varies by policy type |

How to Read Your Policy Documents Without Losing Your Mind

The summary of benefits and coverage (SBC) — the standardized document insurers must provide in the US — is your best friend when comparing plans. It presents key terms in a consistent format, making apples-to-apples comparisons possible. CMS.gov’s health insurance terms guide offers official definitions that match what you’ll find in these documents.

When reading any policy, focus on these five things in order:

- The premium — What does it cost just to have coverage?

- The deductible — What do you pay before the insurer shares costs?

- The copay and coinsurance — How are costs split after the deductible?

- The out-of-pocket maximum — What’s your worst-case scenario?

- The network — Are your doctors covered?

Everything else — formulary tiers, prior authorization rules, referral requirements — matters for specific situations but these five form the financial skeleton of any plan.

A Final Word: The Most Expensive Health Insurance Mistake You Can Make

It’s not choosing the wrong deductible or the wrong network. It’s not even forgetting to use your FSA before year’s end.

The most expensive mistake is not engaging with your coverage at all — just autopiloting into whatever plan is cheapest, never reading an EOB, never checking whether your prescriptions are on formulary, never asking whether a procedure requires prior authorization.

Health insurance is, at its core, a contract. And like any contract, it rewards the people who actually read it.

The terminology exists to describe real mechanisms with real financial consequences. Once you learn the vocabulary, the jargon stops being intimidating and starts being useful — a precise set of levers you can use to make smarter decisions about your money and your health.

You’ve started here. That already puts you ahead.

Quick-Reference Glossary of Key Health Insurance Terms

| Term | Plain-English Definition |

|---|---|

| Premium | Monthly fee to maintain coverage |

| Deductible | Amount you pay before insurance starts covering |

| Copay | Fixed fee per visit or service |

| Coinsurance | Percentage of costs you pay after deductible |

| Out-of-Pocket Maximum | Your annual spending ceiling; insurer covers 100% after this |

| Network | Group of providers with contracted rates with your insurer |

| In-Network | Provider in your plan’s contracted group; lower costs |

| Out-of-Network | Provider outside your plan; higher or no coverage |

| EOB | Explanation of Benefits; shows how a claim was processed |

| Formulary | Insurer’s approved drug list, organized by tiers |

| Prior Authorization | Insurer approval required before certain services |

| Pre-existing Condition | Health condition present before coverage began |

| HSA | Tax-advantaged savings account for medical costs (US, HDHP) |

| Excess | UK term for deductible in private health insurance |

| Open Enrollment | Annual window to select or change insurance plans (US) |

Have questions about your specific plan or health insurance terms in your country? Drop them in the comments — we’ll do our best to translate.